Perpetual Markets Economics and Interest Rate Commentary

Weekend peace talks produce negative outcome but ceasefire still holds. The world economy needs the Strait of Hormuz to reopen soon.

Key points

- News over the weekend from peace talks was unfavourable with no agreement reached and a re-escalation in the war of words. Pakistan is aiming to organise further talks.

- Data remains secondary, with the duration of the Strait of Hormuz’s effective closure remaining the most important consideration for inflation, economic activity, unemployment and monetary policy globally.

- Weekend markets have seen around a US $8 rise in the price of oil following news of the negative result from the US-Iran talks, pressuring weekend equity markets lower. Oil prices are still around US $15 a barrel lower than pre-ceasefire levels as the ceasefire holds and there is still the opportunity for further talks to occur.

- It’s a quiet week for US data, with only secondary data released. Of more interest will be the emerging views of a host of Fed speakers and other central bankers at the IMF World Bank Meetings in Washington about how monetary policy should respond. The latter include three RBA appearances.

- Australian data includes the NAB Business Survey and Westpac Consumer Confidence, both of which should reveal a negative impact from March’s very large rise in oil prices. Labour Force data later in the week is of less relevance, reflecting conditions in effect before March’s developments. Economists expect an unchanged 4.3% unemployment rate, a rate considered too low by the RBA to be consistent with at-target inflation. This allows the RBA to focus on inflation and inflationary expectations in the near term though, the Board must also consider the negative medium-term impacts on activity.

- Markets have repriced to no near-term move in US interest rates (I continue to favour some slight bias to higher US interest rates), while Australian markets have two rate rises priced, though interestingly not at meetings which contain forecast updates. The market is 64% priced for a rate rise at the May meeting. Having increased rates at both the February and March meetings, it would seem prudent to me for the Board to await some further information about Middle East developments, as four members wanted to do in March.

Middle East Developments

The good news of the last week was of course that as the world counted down to President Trump’s deadline for an escalation of the war against Iran and the destruction of civilian infrastructure, a two-week ceasefire between the US and Iran was agreed to, with news that the two parties would negotiate a peace plan in Pakistan over this weekend.

News over the weekend was less favourable, with the two parties unable to reach an agreement after one day of peace talks. Iran described the US as having excessive demands (the US wanted Iran to commit to not develop a nuclear weapon). On Sunday, President Trump once again threatened to bomb Iranian infrastructure and to blockade the Strait of Hormuz. Iran suggested the latter would breach the terms of the ceasefire agreement. Pakistan reportedly will try to arrange new peace talks. It’s not clear from these developments whether the ceasefire will end (with expected market consequences) or whether further talks will be scheduled before the end of the current ceasefire (let’s hope so).

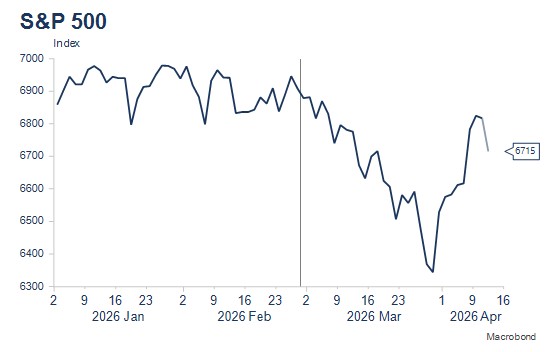

Oil prices, which dropped sharply when the ceasefire was announced and closed on Friday at around US $92.40, basis Brent, have risen 8% or around US $7.40 on IG’s weekend markets, reflecting this lack of progress, but remain $10-15 lower than the pre-ceasefire trading levels. US stock indexes are around 1.5% lower in weekend IG markets. Gold, silver and bitcoin prices are 1%, 2%, and 3% lower over the weekend.

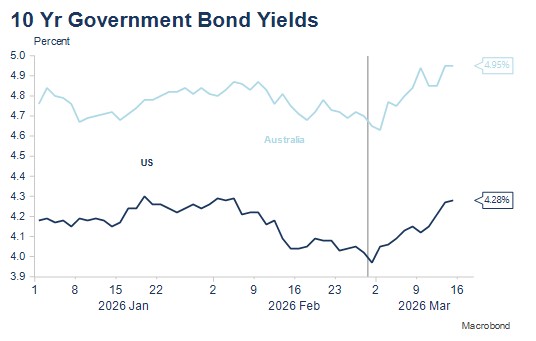

Bond yields have corrected a little lower since the ceasefire lowered oil prices, but ten-year yields remain around 30bps higher than pre-conflict levels in both Australia and the US, reflecting the less favourable inflation environment.

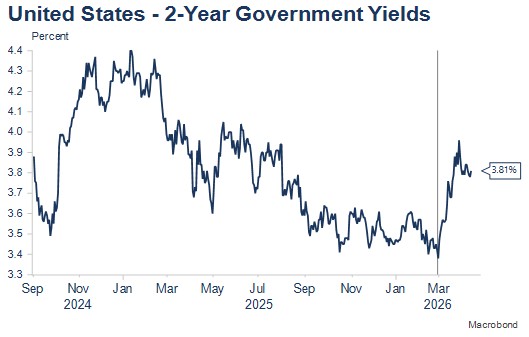

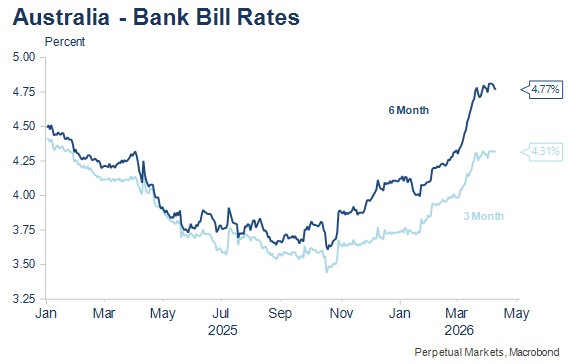

US two-year yields and Australian short-term interest rates are both considerably higher since the conflict, though part of these moves likely reflected repricing of the economic, inflation and monetary policy outlooks, independent of the conflict. The outlook for the US economy was looking more favourable and the inflation outlook less favourable, the latter suggested in ISM price lifts ahead of significant jumps in March. This week’s US inflation prints confirmed a third successive hot core PCE reading (0.4% m/m in February), though the core CPI was a less threatening 0.2% m/m for the second consecutive month.

Outlook

As was the case last week, much depends on:

- How long the Strait of Hormuz remains effectively closed. That will determine the short-term course of oil prices, with an extended closure likely to cause much higher prices, energy shortages and global recession.

- The damage caused to infrastructure, which will determine how quickly energy prices can return toward pre-conflict levels after a resolution is enacted.

- How central banks react to the conflicting inflation and employment pressures caused by the shock, with both of course dependent on points (i) and (ii).

We’ll likely hear more about point three this week when central bankers gather for IMF and World Bank meetings in Washington, though we broadly know:

- Central banks will look through the first-round price spike caused by oil prices and concern themselves with second-round effects, including on inflationary expectations.

- The context is important with inflation having remained above target for four to five years.

Fed speakers last week continued to indicate that a period of observation was prudent and that interest rates were well placed; the latter terminology that reflects the ability for interest rates to be moved either up or down as appropriate. Interestingly, the Minutes again revealed that several members wanted to signal a more two-sided possibility that interest rates are equally likely to increase as decrease, though this was not the view of the majority of FOMC participants. That said, it seems very unlikely that there can be any near-term cut to US interest rates. This has now been priced by US markets, though medium-term there remains around two thirds of a rate cut priced out to mid-2027. My bias is towards some US rate rise pricing being reflected, especially if the conflict in Iran can soon be resolved.

Australian markets continue to price interest rate rises, with almost two full increases priced over the next four meetings. Interestingly, however, the rises are priced at meetings that do not include forecast updates, which is slightly unusual, as the Board usually likes to be informed by the staff’s revised outlook. That said, I tend to agree with the near-term pricing, with a move at May’s Board Meeting only 62% priced. My preference remains that having tightened at both the February and March Board Meetings, there is a reasonable argument for the Board to await further information on how the Middle East conflict may play out in coming months. My broader view is also unchanged that one more interest rate increase this year is probably too little and three interest rate rises is too many, though I am more inclined to one interest rate increase than three.

Economic Calendar – key Australian and US events this week

Throughout the week: IMF and World Bank Meetings and a host of Fed speakers ahead of the Fed communications blackout beginning on Saturday. The views of Waller and Williams are always very important, with further news on the emerging consensus as to how central banks will approach the current energy crisis impacts on inflation of most interest. There’s only secondary US data this week - I remain interested in Indeed job postings trends.

Tuesday 14 April: (8.15am) RBA Deputy Governor Hauser Fireside Chat; Westpac Consumer Sentiment (April); NAB Business Survey (March). Both surveys are expected to show a significant negative reaction to the sharp rises in energy prices over March, with the timing of both surveys capturing most of the energy price rises. The consumer sentiment survey may also capture some of the ceasefire news. I’m not sure how relevant either data point is - for me, the key factors remain how long the Strait of Hormuz is closed and how central banks then respond to the current shock.

Thursday 9 April: (6am) RBA Hauser panel participation. Employment (March) - Bloomberg median +17K; unemployment expected to be unchanged at 4.3%.