Perpetual Markets Economics and Interest Rate Commentary – 8 June 2026

US rate re-pricing on strong data and inflation risks drags Australian interest rates higher. Minimum wage decision not helpful. NAB Survey and US CPI focus this week.

Key points

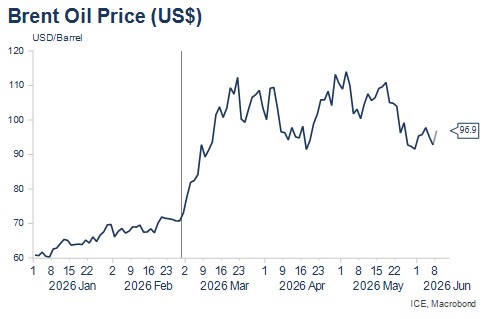

- Another week and still no peace deal. Oil prices have risen only modestly in spite of escalating skirmishes between the US and Iran and continued Israeli operations against Hezbollah in Lebanon.

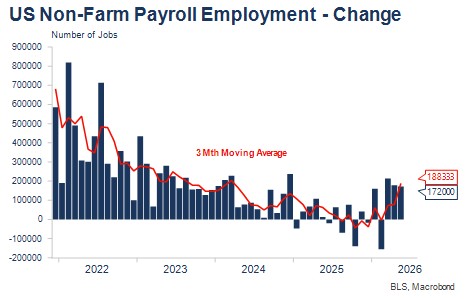

- Equity markets, bond yields and commodities all sold off sharply on Friday following the publication of much stronger than expected May non-farm payrolls figures. The latter should allow those on the Fed concerned about inflation risks to have the upper hand. US markets now discount nearly two full interest rate rises by mid-2027 and one full rate rise by year end. Trading in the early days of this week is likely to continue to be influenced by that release. Our full write up (separately distributed) noted some signal from the NFIB Survey of weaker payrolls growth ahead.

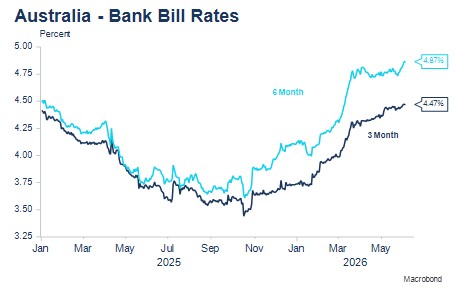

- Australian yields have been dragged higher by US yields, but also by the decision by the Fair Work Commission to grant a larger than expected 4.75% minimum wage rise for next year. At roughly twice the RBA’s target rate of inflation and based on a forecast of inflation that might not be realised, this is poor policy that will make the RBA’s job of returning inflation to target, more difficult.

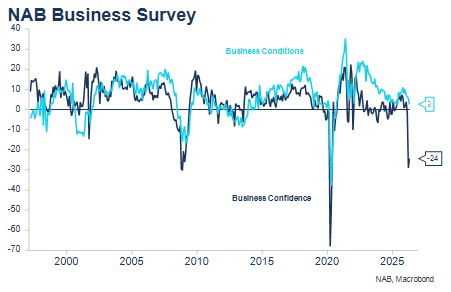

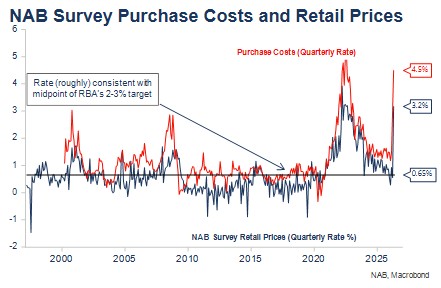

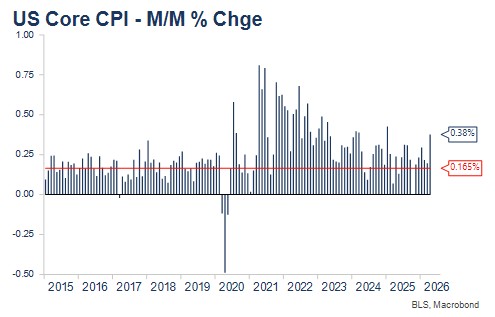

- Key releases this week are the May NAB Business Survey and the US CPI. I’ll be watching the extent to which business conditions continue to deteriorate, with the survey capturing business reaction to the Federal Budget (negative), and how much cost pressures and retail pricing continue to rise. In the US, the May CPI will be important, for the same reason. An outcome above 0.3% m/m would likely continue the repricing of US interest rates. Comments from respondents to the ISM surveys released last week contained very widespread reports of cost pressures.

Market and economic developments in the past week

Despite repeated statements from President Trump that a peace agreement remains under active negotiation and is close, the past week has been characterised by greater military activity between Israel and Lebanon, and isolated skirmishes between the US and Iran. Given the latter, it’s a little surprising that the oil price has only risen around US$5pb over the week. The Strait of Hormuz remains effectively closed.

There were two major economic releases for the week: one each in Australia and the US. Most importantly, non-farm payrolls data for May again surprised sharply to the upside. This led to a significant selloff in US 2-year yields as markets repriced the likely course of Fed policy. Continued low unemployment means FOMC members worried about inflation risks will likely hold the upper hand. Market pricing now reflects nearly two full 25bps interest rate rises by mid-2027, with a full rate rise now discounted by the end of this year. Last week, only a 60% chance of a rate rise was factored by the end of the year.

Australian interest rate market pricing was dragged higher by the sharp rise in US yields on Friday. Before then, yields had also drifted slightly higher, particularly after the granting of a higher than expected 4.75% minimum wage increase for next year. The Fair Work Commission chose to match the minimum wage increase with the RBA’s forecast of headline inflation.

I view this a poor policy choice, which will make the RBA’s task of returning inflation to target a little harder. The main reason Australia inflation remains above target appears to be the tight labour market and elevated wages, together with housing market pressures, though the latter seem to be easing somewhat in the wake of recent interest rate rises and budget decisions on housing taxation.

The week ahead – key Australian and US events

It’s a quieter week for data in both the US and Australia, though there will be interest in the policy decisions of the Bank of Canada and European Central Bank. At the end of the week SpaceX IPOs.

Monday 8 June – Public holiday (Australia).

Tuesday 9 June – Westpac Consumer Sentiment (June); NAB Business Survey (May).

Wednesday 10 June – $1bn 4.75% 2037 bond tender; (overnight) US CPI (May); Bank of Canada (no change in policy expected).

Thursday 11 June – Consumer inflationary expectations (June); ECB (25bps rate rise expected).

Friday 12 June – (overnight) University of Michigan 1-year and 5-10-year inflationary expectations; SpaceX IPO.

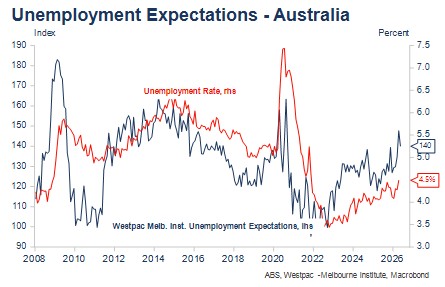

Two releases will likely capture most attention: the NAB Business Survey on Tuesday, where I’ll be watching to see the extent to which business conditions have continued to deteriorate (very likely in the wake of an unpopular budget), as well as the indications of both input cost pressures and retail price response, both of which were very elevated in April. The unemployment expectations component of the Westpac Consumer Sentiment release (also on Tuesday) is always worth monitoring as it provided important early warning of unemployment trend changes during the COVID period.

In the US, the May CPI is the key release, especially as continuing very low unemployment is likely to allow the FOMC to focus on inflation risks in much the same way as the RBA has been able to do in Australia. The market is looking for a 0.3% core CPI outcome (2.9% y/y up from 2.8% y/y in April). Monthly rates of this quantum remain much higher than the 0.165% monthly average required to annualise at the Fed’s 2% inflation target. Markets appear to have finally got that message after the strong May payrolls figure and now discount nearly two tightenings by mid next year.

There may well also be greater interest in Australian and US inflationary expectations readings (Thursday and Friday, respectively) after RBA Monetary Policy Board member Harper noted in a speech during the week that the Board was closely monitoring an increase in the three-year inflation expectation derived from market pricing.