Perpetual Markets Economics and Interest Rate Commentary – 27 April 2026

A huge week for data and events. Q1 Australian CPI to confirm RBA had more work to do before the war in the Middle East. The impact on activity suggests it might be more prudent for the RBA to await further information.

Key points

- The Strait of Hormuz remains effectively closed. Oil prices reversed last week’s rally, though Australian interest rate markets were relatively unmoved, and are still attaching a 77% probability to a further rate increase at the May RBA Board meeting. The longer the Strait remains closed, the greater the risk of global recession. US interest rate markets continue to remove near-term easing expectations, with more of this trend to be expected. The Manufacturing ISM is released on Friday night. This suggested greater inflationary pressure even before the recent surge in energy prices.

- It’s a huge week for data and events. The Q1 CPI is expected to confirm that Australian inflation was running too hot before recent Middle East events. In the absence of the latter, further tightening in May would be a lay down misère. But with a significant impact on activity likely from higher energy prices and an unknown duration Strait of Hormuz closure, the sensible approach would seem to be to wait for more information. That is unless the Board felt it wanted to get back to 4.35%, before Middle East developments. With four members voting to wait in March, 77% confidence in a May tightening seems too high.

- With little data released capturing the “shock” period, liaison evidence is likely to play a very important role in the May decision. This is likely to be quite negative for activity in many aspects, which should reduce medium-term inflation concerns if the oil price is sustained at higher levels. Ordinarily, it would be inconceivable for the RBA to tighten given the March and April prints for consumer and business confidence.

- There are no less than five central bank meetings this week, including the Fed. I’ll be looking for common themes emerging from these meetings. While looking through the initial price shock and concentrating on impacts on inflationary expectations has been a common refrain, so too has been the starting point for interest rates and inflation relative to target (the inflationary context).

- On top of all that, five of the Magnificent Seven report Q1 earnings and will likely guide on AI expenditures. A raft of other Wall Street megacaps also report and may provide guidance on the response of consumers to the oil shock.

Middle East and market developments

The oil price is broadly back to where it was around ten days ago at US$106 per barrel (Brent). The Strait of Hormuz reopened for only a few hours last weekend and has been effectively shut since. There have been no outward signs of progress in peace talks, with the latest planned meetings called off by the US over the weekend. This means the world oil market continues to receive 20% less oil supply per day.

As we have written in previous weeks, if this situation persists for several months, the implications for business costs and economic growth are likely to be severe, with resultant much higher oil prices and potential supply interruptions likely to cause at least a short-lived supply-side recession around the world, while supplies remain restricted. AI investment spending will be an important cushion.

The situation could quickly reverse if the Strait of Hormuz reopens and supply is restored or morph from a supply-induced temporary recession into a full balance sheet recession if central banks are heavy-handed in their monetary policy reactions. Forecasts of three further interest rate rises in Australia this year seem too bearish if oil prices remain high.

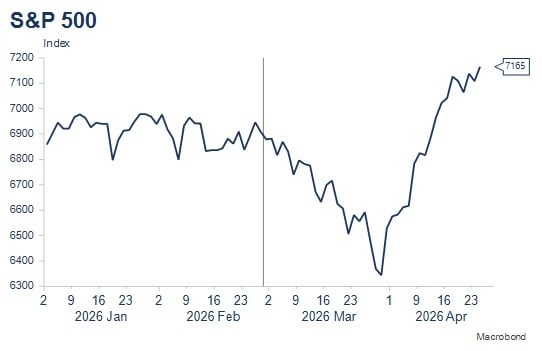

Share markets seemingly remain unfazed with the S&P500 reaching another record high during the week. This likely reflects a combination of reasonable corporate earnings results, an expectation that the Strait of Hormuz closure will not be an extended one, and optimism that AI will drive strength in near-term earnings for technology companies, but in time, more broadly across the corporate world.

The Fed meets on Wednesday (announcement 4am Thursday, AEST), with no change in interest rates widely expected. Any change in the votes (all but one FOMC member last meeting voted for no change) or communication in Jerome Powell’s last scheduled press conference as Fed Chair (he may stay on temporarily if incoming Chair Warsh is not confirmed ahead of the next meeting) will be important. There is a core group of Fed members suggesting no change in interest rates is the best approach in the current uncertain environment, some wishing to indicate that the next move could equally be up or down, Governor Miran favouring immediate easing, and Governor Waller remaining concerned about potential weakness in the labour market. A number of technology companies announced further large job cuts last week to fund AI investment.

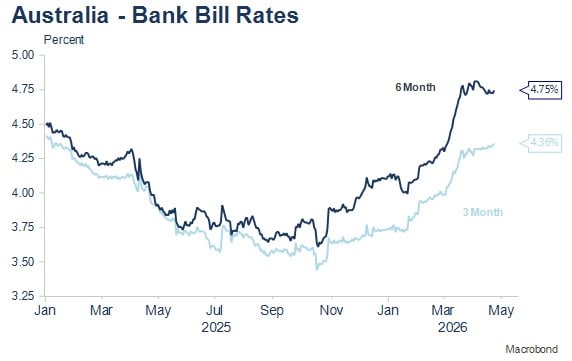

Despite the sharp rise in oil prices, Australian short and longer-dated yields were relatively unchanged over the week, with three and six-month bills ticking three basis points higher. The markets remain 77% priced for a further tightening by the RBA at the May Board meeting (unchanged from last week) but have increased their pricing above 100% for a move by the June meeting, implying a very small chance of back-to-back moves. I think the latter is very unlikely and prefer a June rise over a May one. Australian markets price two rate hikes over the next four meetings, with peak pricing of two and a half rate increases, consistent with the view that three rate hikes would be too aggressive.

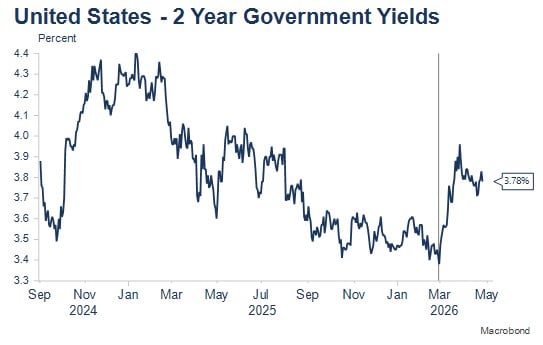

US short-term yields have continued to reduce and defer pricing of further interest rate reductions by the FOMC. Whereas last week a full rate cut was priced by July 2027 and nearly two thirds of a rate cut this year, now only two thirds of a rate cut is priced by July 2027. This saw 2-year yields rise modestly over the week.

The continued strength in the US share market and support from tech spending is an activity argument against further easing, while inflationary pressures were already beginning to emerge even before the Middle East energy price shock. Weekly ADP employment data has strengthened in recent weeks, and while we receive an important update on the Manufacturing sector with the April ISM on Friday, April non-farm payrolls is not published until May 8. Other important US data includes Q1 GDP, Q1 ECI and March PCE data overnight on Thursday. Recent PCE data was running a little hot even before the recent jump in fuel prices. With the market expecting a 0.3% m/m outcome, this would suggest a further reduction in pricing for US easing.

Economic calendar – key Australian and US events this week

It’s a huge week for economic data and events. The Fed meets (along with the Bank of Japan, Bank of Canada, Bank of England and ECB), Australia’s March and Q1 CPI are published, important precursors to next week’s RBA May Board Meeting, as well as a raft of US earnings reports. US GDP, PCE inflation and ECI wages data are also out as well as the important Manufacturing ISM for April, the latter an important guide as to the impact on activity from the sharp rise in oil prices.

Tuesday 28 April: $1bn, 4.25% 2035 bond tender, Bank of Japan meeting.

Wednesday 29 April: Australian March and Q1 CPI (see later section for CPI and RBA commentary). Overnight: FOMC Meeting (4am); Powell Press Conference (4.30am). No change in US rates expected. Microsoft, Amazon, Alphabet and Meta report. Bank of Canada meeting.

Thursday 30 April: Overnight” US GDP (Q1), ECI (Q1) and PCE (March). Apple reports. ECB and Bank of England meetings.

Friday 1 May: $1bn 4.5% 2033 bond tender. Overnight: ISM Manufacturing (April).

Australian CPI preview and RBA thoughts

The market is expecting an unchanged 3.3% y/y March core CPI outcome. It’s a little early for the huge (33%) rise in oil prices in March to have impacted the trimmed mean. The 3.3% y/y forecast is equivalent to a monthly trimmed mean of 0.3% m/m. That’s too high as the trimmed mean needs to average just above 0.2% to annualise at the RBA’s 2.5% target.

The median quarterly trimmed mean CPI forecast is for 0.9% q/q, unchanged from Q4. Both the monthly and quarterly trimmed means confirm that Australian inflation was running noticeably above the RBA’s target even before recent Middle East developments, with Deputy Governor Hauser recently characterising core inflation as running around 3.5% (I assess closer to 3.25%). The rise in petrol prices will likely bias this quarter’s result up from a 0.8% q/q outcome. Even discounting this, the RBA had a bit more tightening to do before energy prices rose. The headline CPI is expected to increase 1.4% q/q, jumping to 4.8% y/y from 3.7% y/y, driven by a 33% jump in petrol prices in the month.

RBA Deputy Governor Hauser gave a few clues as to how the RBA staff might advise the Board about current inflation developments in a panel appearance at the end of the previous week. He noted that: (i) interest rates needed to be set high enough to bring inflation back to target (they probably are not there yet); (ii) the central bank needed to respond to signs of second-round inflation or increases in inflationary expectations, though it was too early to have seen much evidence of these; and (iii) the Bank’s staff would be busy assessing whether the related demand shock would reinforce or substitute for further interest rate rises.

In the absence of the significant lift in energy prices in March and April, I would expect the RBA Board to decide to make a further rate increase in May. This would make it more certain that inflation would return to target and possibly shorten the time to return to target in from the mid-2028 timeframe forecast in February.

While March and April fuel price developments clearly worsen the near-term inflation picture, the activity impact will likely also be significant given the size of the increase in fuel prices. This will take some time to play out in the data, meaning that the RBA’s liaison evidence will likely be very important in May’s decision, especially given the limited activity data that has been released covering the shock period. At times like this, the economic data will be a long way behind the economy. The two pieces of evidence that we have seen have been consumer and business confidence, both of which recorded very sharp falls. Ordinarily, it would be inconceivable to imagine the RBA tightening policy in the face of such falls.

My opinion remains that too much is priced in for May, given the unknown duration and magnitude of the current energy shock. If the Strait of Hormuz remains closed, the RBA may be dealing with a recession and wanting to cut interest rates in a few months. If there is a quick reopening, then a return to tightening to combat current above-target inflation would seem sensible. For now, the prudent thing to do would seem to be to await more information. With the Board voting 5-4 to tighten in March, the possibility of a 5-4 or larger vote in the other direction in May is not negligible. Either way, expect a press release and press conference that is hawkish on inflation but uncertain on the impact on the economy.