Perpetual Markets Economics and Interest Rate Commentary – 18 May 2026

The economic outlook remains hostage to Middle East developments. RBA and Australian labour market in focus this week. US and global interest rates continue to develop bearishly.

Key points

- Another week and not much change in the Middle East with very few ships transiting the Strait of Hormuz, ceasefires mostly holding and little progress that can be observed on negotiations between Iran and the US, though discussions remain ongoing.

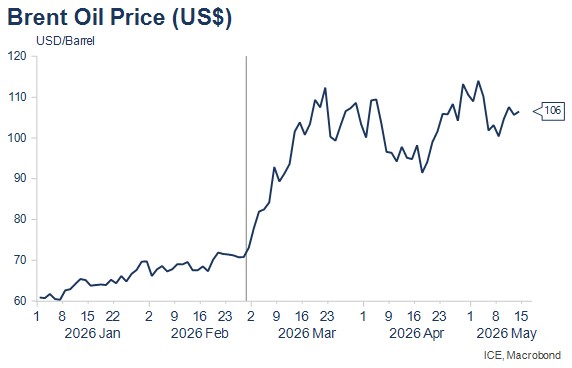

- Bond yields have risen relatively sharply around the world in the wake of higher inflation prints, a continuing shift to the US market pricing in the risk of an interest rate rise and oil prices rising modestly over the past week.

- Australia’s budget seems like it adds to the risk of a pause by the RBA in June, with changes to capital gains tax and negative gearing further impacting weakening sentiment in the housing market. However, global developments suggest this should be traded as outperformance versus the US, rather than expecting any decline in Australian yields.

- The two most important questions that I would like to know the answer to are: 1) how long will the Strait of Hormuz remain closed; and 2) will AI destroy significantly more jobs than it creates, and over what timeframe?

- It’s a very quiet week for US data, with most interest in the FOMC Minutes on Wednesday night, which will likely see the trend to pricing in the risk of US interest rate rises continue. In Australia, the RBA Minutes and a speech by Assistant Governor Hunter on Tuesday will be examined for any further clues as to whether the RBA has the “space” the Governor indicated to observe developments in the economy and inflation for a while. The latter would likely see interest rates unchanged in June (my core view).

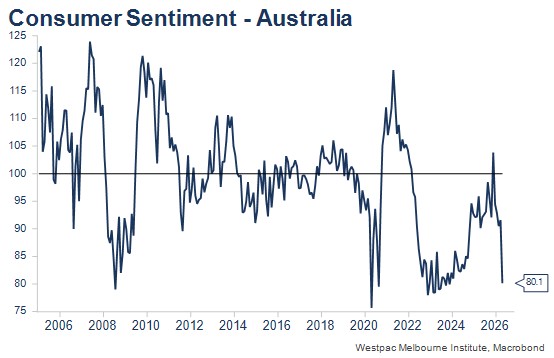

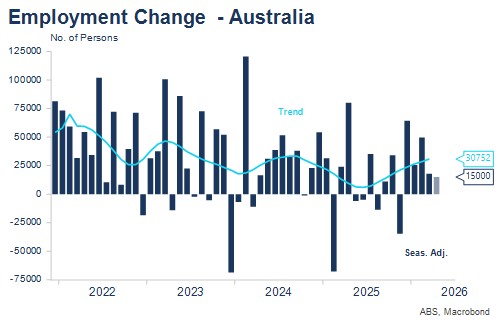

- Elsewhere, consumer confidence should remain very weak in May, while there seems downside risk to employment in April given the sequence of Easter, school holidays and ANZAC Day. That shouldn’t affect the unemployment rate as the participation rate should also adjust. Job ads are not suggesting much change in the demand for labour or the unemployment rate yet, though that should develop if oil prices remain elevated.

The week ahead – key Australian and US events

Tuesday 19 May: RBA Assistant Governor Hunter speaks (9.25am); Westpac Consumer Sentiment; RBA Board Minutes.

Wednesday 20 May: US FOMC Minutes (4am Thursday, AEST).

Thursday 21 May: Australian Labour Force (April).

It’s a very quiet week on the US data front, with only second tier data released. There are speeches scheduled from four different FOMC members, with Governor Waller the most influential in terms of his monetary policy thoughts. We did hear from him last week, at which time he indicated that monetary policy should remain restrictive for some time and that any interest rate cuts would require clearer evidence of disinflation which seems most unlikely in the near-term.

This saw markets continue to shift away from pricing easing in the US, and a full interest rate rise is now priced for the March meeting of 2027. The Minutes on Wednesday night will likely continue this shift given the debate over a change to a neutral bias is likely to feature.

The RBA May Board Minutes and Assistant Governor Hunter’s speech on Tuesday will be examined closely for clues as to whether the RBA will remain on hold in June (less than a 20% chance of a fourth successive interest rate rise is priced). The pricing reflects the suggestion from the Governor that the three recent interest rate rises had created some “space” for the Board to observe developments in the economy and inflation for some time. My expectation is that the Board will hold.

Australian consumer confidence plunged in April as energy prices surged. While the government has temporarily reduced fuel excises lowering petrol prices, the further interest rate rise in May and changes to capital gains taxes and negative gearing announced in last week’s budget will likely see sentiment remain very weak, and perhaps weaken even further.

Labour force data is the other key Australian event this week (on Thursday). This survey is one of the hardest to forecast. The Bloomberg economist median forecast is for a moderate 15,000 rise in unemployment and an unchanged unemployment rate of 4.3%. My bias is to expect a weaker employment outcome as in recent years, many firms and/or employees with flexible work arrangements seem to be temporarily reducing employment over school holiday periods. This April saw school holidays in many states fall between the Easter and ANZAC Day holidays. Any effect on employment should also be reflected in a drop in labour force participation, meaning the unemployment rate is not affected by the holiday calendar.

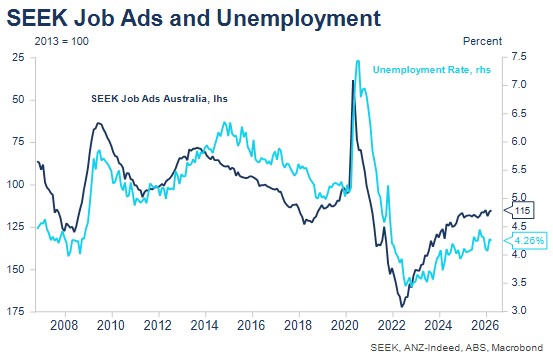

The unemployment rate pleasingly remains very low in Australia at 4.3%, but this is likely a large part of the reason for inflation remaining above the RBA’s 2.5% target. The trend in job ads over the past year and in recent months has yet to signal any significant change in employment demand, though one would expect this to emerge over time if fuel prices remain very elevated or rise further.

Middle East developments

Another week and the Strait of Hormuz remains effectively closed, with transits at a very small fraction of pre-conflict rates. Ceasefires remain mostly in place though there are also attacks occurring from time to time. Oil prices have risen a little from last week, but price levels implicitly reveal the markets expect some resolution to be reached in the next month or so, before supply interruptions overwhelm emergency fuel supply releases and much higher oil prices result. While it’s hard to believe that the Strait of Hormuz might remain closed for a further three to six months, that possibility needs to be considered as much, much higher energy prices, rationing and interruptions to activity as occurred during COVID, would likely result. In that environment, central banks would cease raising interest rates and some emergency interest rate cuts might be considered.

![]()

Interest rate market developments and pricing

There have arguably been two, perhaps three, key interest rate developments over the past week.

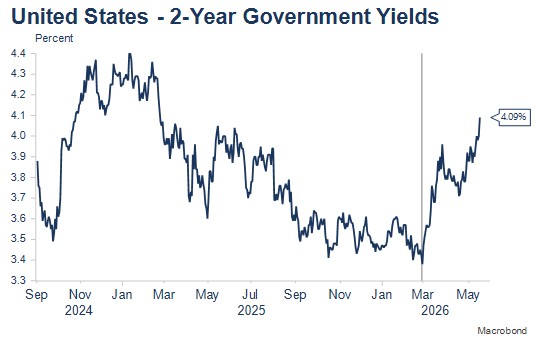

First, US markets have continued to remove the pricing of possible further interest rate cuts and instead price the increasing likelihood that the next move in US interest rates is a rise. A full interest rate increase is now priced by the March 2027 FOMC meeting, and US 2-year yields have risen nearly 20 bps over the past week.

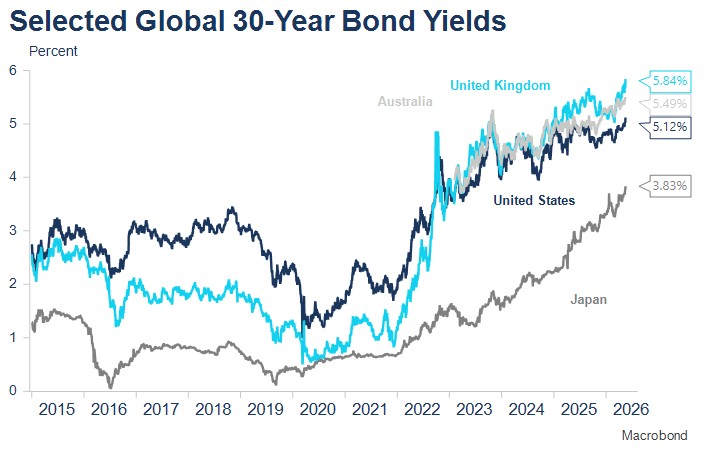

Second, ultra-long bond yields have continued increasing around the world. Higher inflation readings published during the past week (including for the US and Japan), evolving pricing for interest rate rises in the US, renewed rises in oil prices, and lack of progress in peace negotiations likely all contributed.

Long bond yields are important for equity valuations and while the US market has seemed largely immune to all manner of challenges in recent months, higher yields appeared to impact pricing towards the end of last week.

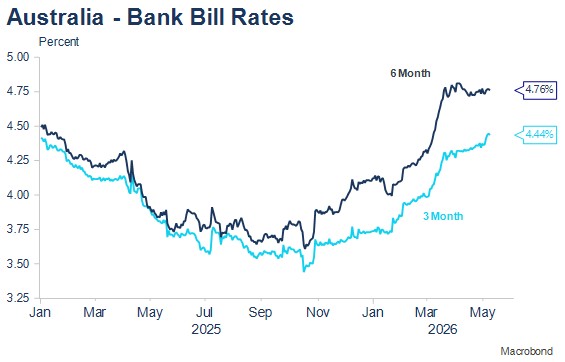

The third potential important development – perhaps more of an important reminder – is that Australian interest rate direction is always very influenced by US and global interest rate trends. So, while the tax changes contained in the Australian budget and the lack of further cost-of-living support seemed likely to support short-end Australian pricing, changes to US short and long end yields mean that the Australian short end pricing now reflects a higher peak for Australian cash rates. The market has slightly reduced the probability of another rate rise in June (to below 20%), though a rise in August is 88% priced and more than fully priced by the September meeting. Peak pricing is now for 1.6 interest rate rises in December 2026 and February 2027, up from 1.4 rate rises priced this time last week.

Outlook

The two most important questions that I would like to know the answer to are: 1) how long will the Strait of Hormuz remain closed; and 2) will AI destroy significantly more jobs than it creates, and over what timeframe?

The first question will determine whether we are dealing with a scenario of much higher oil prices and significantly weaker growth (an extended closure), which is unlikely to see much if any further interest rate tightening required (the combination of higher oil prices and higher interest rates doing the tightening), while a quick resolution would likely see the outlook revert to a core scenario of a long, slow tightening cycle emerging over the next twelve to eighteen months.

The AI investment boom is supportive of that core scenario in the near term but threatens the need for more significant interest rate support in the medium term (beyond two years), if indeed there are widespread job losses.