Perpetual Markets Economics and Interest Rate Commentary – 15 June 2026

RBA preview: risk of further rate increase now looks under-priced. US markets unlikely to re-establish easing pricing even with peace deal, due to short-term inflationary AI boom.

Key points

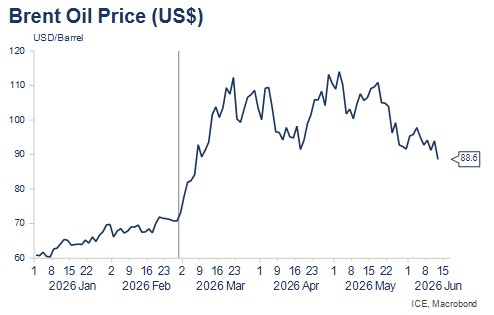

- The peace agreement between the US and Iran has been confirmed by both sides, with signing and the reopening of the Strait of Hormuz scheduled for Friday. This removes an important source of inflationary pressure and should allow more favourable economic conditions to re-establish as the AI investment boom rolls on globally.

- Those conditions are still expected to be moderately inflationary in the near to medium term, preventing interest rate cuts any time soon and still suggesting risk to interest rates remain to the upside. Ongoing attacks between Israel and Hezbollah remind there is an important third actor in the Middle East even as the US and Iran agree on a path forward.

- There are a huge number of central bank meetings this week, including the RBA on Tuesday and the FOMC on Wednesday. With no change in interest rates expected at all meetings except for the Bank of Japan on Tuesday, the focus will be on the text of statements and commentary at subsequent press conferences. This includes the first press conference of new Fed Chair Kevin Warsh overnight on Wednesday.

- Three of the four major Australian banks are now predicting Australian cash rates have peaked, with cuts likely to occur in 2027. The emerging softness in the housing market, accentuated by recent budget taxation changes, is a key factor in these changed views.

- It seems premature to call the next move in Australian cash rates as down, especially given ongoing low unemployment and the recent much bigger than expected minimum wage decision, which will make it harder to deliver 2.5% inflation any time soon. The RBA is unlikely to countenance or signal potential interest rate cuts anytime soon, given the premature easing of 2025.

- There’s no Australian data and little US data of note this week. Next week we see the monthly CPI, the Labour Force data (which I expect to significantly reverse last month’s surprise prints attributable to the unusual sequence of Easter, school holidays and ANZAC Day) and the latest Household Spending Indicator.

- In the short-term, shorter-dated interest rate instruments and bond yields should both benefit from likely lower oil prices from a peace agreement. My base case, however, remains of a long, slow tightening cycle in both Australia and the US as the AI investment boom rolls on globally.

Market and economic developments in the past week

Oil prices have fallen again over the past week, dropping around US$8pb as expectations remained high that a peace agreement would be signed very shortly and have dropped further today on confirmation of this. Continuing conflict between Israel and Hezbollah reminds that Israel remains an important third actor in the conflict even as the US and Iran agree on a path forward.

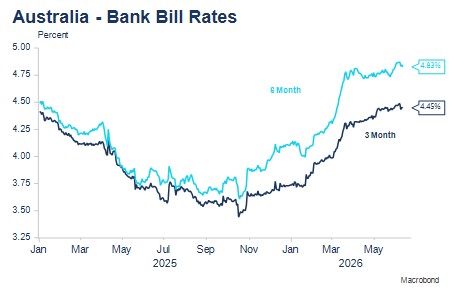

Shorter-term interest rates and bond yields in both Australia and the US have dropped again over the past week, with lower oil prices and a possible peace deal removing one important source of inflationary pressure. In Australia, markets further reduced the pricing of interest rate increases and three of the four major Australian banks now forecast that cash rates have peaked, and the next move will be rate cuts in 2027.

Markets now price just over a 50% chance of one further rate rise by the RBA by early 2027. That appears to understate that likelihood, especially given the minimum wage decision.

RBA preview

The RBA Monetary Policy Board meets on Monday and Tuesday this week, with any policy change to be announced at 2.30pm on Tuesday. I expect the RBA to leave interest rates unchanged in June. This is the unanimous expectation of market economists, while financial markets price exactly a zero chance of an interest rate rise at this meeting.

After increasing interest rates in February, March and May, the Board clearly signalled that these moves had created space to observe the impact of the tightening of policy on the economy and inflation as well as developments in the Middle East conflict, for some time.

Since the May board meeting:

- The unemployment rate recorded a surprise increase from 4.3% to 4.5% as employment declined 19,000 in April.

- Trimmed mean inflation remained above the 2.5% target, rising from 3.3% to 3.4% in April. Inflation has remained stubbornly but not hugely above target, with the Middle East conflict boosting headline inflation significantly in recent months.

- GDP was weaker than expected at 0.3% q/q in Q1, but around expectations at 2.5% y/y (and not as weak as the headline results suggest due to cyclones and bad weather notably affecting exports and related transport services).

- The Fair Work Commission granted a considerably larger than expected 4.75% minimum wage rise from 1 July 2026, almost twice the 2.5% RBA’s inflation target.

- The Federal Budget introduced significant changes to taxation for negative gearing and capital gains, with considerable implications for the investor housing market.

- Independent Monetary Policy Board member Ian Harper highlighted the importance of increasing medium-term inflationary expectations in an otherwise unnoteworthy speech.

- The NAB Business Survey measure of capacity utilisation has declined for two months in succession.

- Three of the four major Australian banks have changed their forecasts and now suggest the cash rate has peaked at 4.35%, with interest rates set to fall in 2027. Westpac continues to forecast an interest rate increase at both the August and September board meetings, though back-to-back rises in such short order after three recent interest rate increases seems very unlikely, especially as one source of inflationary pressure seems very likely to substantially dissipate in the near future with a peace deal reported to be very close to signing. I’d expect a change in their forecast shortly.

What to watch for

With monetary policy decision statements typically relatively short and containing little in-depth information or analysis, most focus will be on the Governor’s Opening Statement to her 3.30pm press conference on Tuesday, plus answers given to journalists’ relevant questions.

Market participants will be looking for clues as to how long the RBA might remain on hold, the possibility and circumstances under which the next move in interest rates might be a cut, how the RBA is interpreting weakness in the housing market, the Bank’s take on the latest unemployment numbers (it’s a volatile and unreliable number on a monthly basis - with a further update next week likely to reverse much of April’s apparent weakness) and any further comments in relation to the rate of inflation, with the implications of the 4.75% National Wage Case award of particular interest.

The influence of housing markets on monetary policy

The banks that suggest the next move in interest rates will be down, appear to have been heavily influenced by emerging softness in the housing market, which will likely be accentuated by the impact of recent budget tax changes. These changes reduce the amount that investors can borrow by around 10-20%, which will lessen investor demand and capacity to pay and therefore likely also prices, though first home buyers continue to receive significant government support. The impact on rents from the changes is less clear. Rentsare an important component of the CPI.

Of course, as the RBA has repeatedly discussed, the Bank does not target house prices, though the housing market has other important impacts both directly and indirectly for the economy and monetary policy. Housing is typically an important leading indicator for the general economy, while wealth effects from housing can also be important for the strength of consumer spending. Other important indirect effects include the effects on inflation from rents and newly constructed dwelling prices, two very highly weighted components of the CPI.

Conclusion

The combination of a peace deal and some softness in the housing market remove the need for any further near-term tightening by the RBA Board, though the National Wage Case decision and continuing low unemployment rate mean any quick move to thoughts of easing is very premature and the risk remains of some further tightening, with the Q2 CPI still important.

Markets now price just over a 50% chance of one further interest rate rise by early 2027, which looks to understate that probability. My base case remains of a long, slow tightening cycle driven by inflationary pressures related to the AI investment boom and associated data centre rollout, which is causing strong demand for semi-conductors, water, electricity and copper.

Businesses and consumers alike will welcome the near-term reprieve from both interest rate increases and high fuel prices, though many businesses will still have to cope with additional pressure from an irresponsibly large minimum wage increase in the circumstances, particularly for the Retail and Hospitality sectors. This will complicate the RBA’s task returning inflation to target.

The week ahead – key Australian and US events

It’s a very quiet week for data in both the US and Australia allowing focus on important central bank meetings globally including in Australia and the first FOMC meeting with Kevin Warsh as Chair. Focus will be on a likely change in bias to neutral in the US, changes to the “dot plots”, with FOMC participants expected to factor no interest rate cut this year (down from an expectation of one further cut in the March Summary of Economic Projections). There will be interest in the number of participants that pencil in a rate increase this year, and it seems a reasonable likelihood that some will. The continuing AI investment boom suggests US interest rate markets will not re-establish easing pricing, which will likely be a moderate ongoing negative for Australian bond market pricing after a likely near-term peace “dividend” rally.

Monday 15 June: US Iran peace agreement announcedsigned. (overnight) US Industrial Production and Capacity Utilisation.

Tuesday 16 June: RBA cash rate announcement (2.30PM); Bank of Japan interest rate announcement (25bps increase expected).

Wednesday 17 June: (overnight) Riksbank policy decision; US Retail Sales (May); FOMC interest rate announcement (4am, AEST – no change expected); Fed Chair Warsh first press conference (4.30am, AEST).

Thursday 18 June: NZ GDP (Q1); Swiss National Bank, Bank of England and Norges Bank policy decisions (no changes expected).

Friday 19 June: US Iran peace agreement to be signed and Strait of Hormuz to reopen.